Ahmed was sipping his coffee while paying a few bills, purchasing flight tickets for his next holiday, and reviewing his finances without letting his coffee get cold.

Let’s rewind a few years.

To complete the same tasks, Ahmed would have needed to make a few trips to the banks and navigate through a lot of paperwork.

Thanks to the rapidly changing digital landscape, banking and payments have been evolving fast. Open banking is a product of this changing landscape, redefining how businesses and financial institutions interact. In this article, we’ll dig deep to understand more about it.

What is Open Banking?

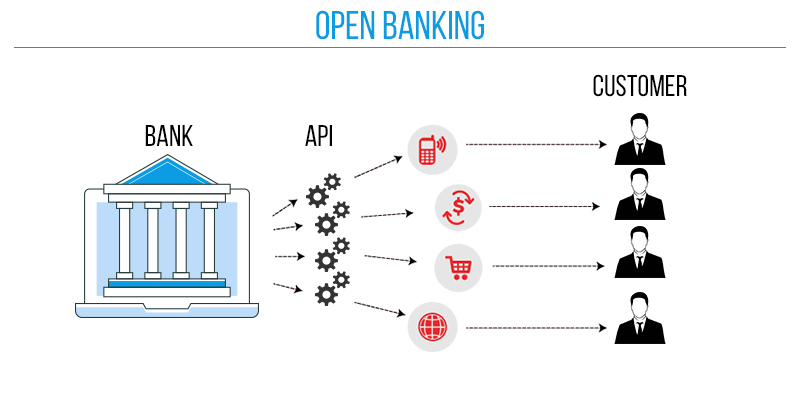

Open banking is an evolving practice where traditional banks securely share customer data with third-party financial service providers through APIs. Traditionally, consumer banking data was only available to consumers and their respective banks.

However, open banking allows banks to share consumer data with financial services providers such as fintech, merchants, digital platforms, or currency exchanges.

While open banking offers promising gains, like real-time payment, it also carries risks as more consumer data are shared widely.

What are the Key Components of Open Banking?

An open banking system works like an ecosystem with multiple components, each helping and benefiting from the others. Let’s examine each of these.

APIs (Application Programming Interfaces)

Application programming interfaces (APIs) let different software applications communicate with each other, even if they are built by different organizations. Open banking heavily relies on APIs to securely share financial data between banks and other financial institutions so that customers can access innovative financial services like budgeting tools, paying bills on the go, or comparing loans from different sources.

Third-Party Providers (TPPs)

Third-party providers (TPPs) are external financial institutions authorized to access consumers’ financial data from the bank. TPPs integrate with banks’ APIs to offer various financial services, such as budgeting tools, loan comparison tools, or payment services.

Data Sharing

Finally, there’s data sharing, where banks share consumer financial data with authorized TPPs through APIs in secured environments. Consumer consent is a must for data sharing, as sensitive information like transaction history, account information, and similar financial details are shared. Various regulations and compliances are in place to ensure safe data sharing between the authorized parties.

What are the Benefits of Open Banking?

Open banking benefits customers, banks, and businesses alike. Let’s see how.

1. For Consumers

Consumers are already reaping the benefits of open banking by increasing access to innovative financial services. By sharing their financial data, customers are accessing tailored products that make their lives convenient.

For example, unified financial data can be used to offer customers useful tips on managing personal finance or recommendations on where to place savings for better returns.

Open banking gives customers more control over their personal data. For example, the APIs are so designed that only YOU can access the login details. And unless you share those login details with anyone else, no one can access them. Customers can also control who can access their financial data and to what extent. For example, companies can only take payment when the customer approves it.

2. For Banks and Financial Institutions

Open banking has benefited consumers and opened up new revenue streams for banks and financial institutions.

As banks and financial institutions have access to more customer financial data, they are in an advantageous position to derive better customer insights, which will help them create more targeted and tailored financial solutions.

Allowing new players in the industry fosters competition, so we can only expect fierce competition among new fintech startups. This will lead to better, more innovative products with competitive pricing for consumers.

3. For Businesses and Merchants

Open banking has made it convenient for businesses and merchants to streamline the payment process. With access to better financial products and services, businesses can offer better customer experience.

For example, by partnering with payment solutions like PayBy, businesses can integrate payment gateways to offer various cashless payment methods to diverse customer payment preferences.

So, if you’re an e-commerce platform, you can integrate different payment options, such as credit and debit cards, wallets, etc., for easy checkout.

If you’re a gaming company, you can make it easy for players to load funds into your gaming or betting platform, allow players to monitor their spending, and have complete control over their funds.

How Open Banking Transforms Payment Gateways

Open banking has many benefits for payment gateways. For example, it ensures faster transaction time with better security and reduced costs and fees. This ultimately results in a better customer transaction experience.

1. Improved Payment Efficiency

Since open banking allows financial data sharing, payments can happen in real-time through payment gateways with increased efficiency. For example, PayBy is designed to handle all end-to-end payments, making it easy for businesses to process and record every transaction. It’s also cost-effective, as you need to pay only a small fee for setup charges and chargebacks.

2. Enhanced Security and Fraud Prevention

Open banking has been pivotal in enhancing security and fraud prevention for payment gateways. For example, today, we have biometric authentications for payments that enhance security, reduce fraud, reduce identity theft risk, and improve user experience. Some common biometric applications in payments include iris recognition, facial recognition, fingerprint scanning, and tokenization with biometrics.

Open banking has also made it possible to set up real-time continuous monitoring of accounts so that you are alerted whenever there is any unusual financial behavior in your account. This helps you detect potential fraud immediately and take necessary action.

3. Personalized Payment Solutions

Powered by open banking, merchants can offer customers their preferred payment options based on the user’s past data. For example, with PayBy you can choose payment gateways that allow the consumer to choose their preferred payment mode. These could be credit/debit cards, UPI payments, or mobile wallets.

You can easily integrate your payment processing system with other financial services. For example, you can offer in-app payments by integrating your payment gateway into the app for faster payment processing or integrating with your website.

Common Challenges of Open Banking

While open banking has redefined how banks and financial institutions used to work, giving convenient access to financial data, it has also raised some serious risks.

1. Data Privacy and Security

Open banking APIs are not completely risk-free. As data becomes more interconnected, there are potential threats of data breaches, hacking, or unauthorized access to a customer’s account through a malicious third-party app. Thus, it becomes extremely important for financial institutions and merchants to keep the customer’s sensitive information safe.

Building trust with customers is another area of concern. Customers need to be completely satisfied with any third parties who will be accessing their sensitive information. A recently conducted survey around the world showed that more than half of the participants were concerned with their data privacy. This is a serious concern that needs to be addressed.

2. Regulatory and Compliance Issues

Various regulations, like PSD2, GDPR, etc., are in place to ensure data safety, and all open banking platforms must adhere to these regulatory requirements. However, keeping up with constantly changing regulations and adhering to compliance norms consistently across different regions is challenging.

Failing to do so can result in heavy penalties, lawsuits, and reputational damage. Financial institutions that can understand their regulatory landscape, anticipate any change, and move swiftly to accommodate the change will have competitive advantages over other players.

3. Technical and Operational Hurdles

Operating in an open banking platform requires significant high-level technology investment. For example, the APIs deployed by banks or third-party providers must work properly and support various environment configurations. Failing to do so can create downtime and operational hurdles.

Scalability is another area of concern. For example, many traditional banks that use legacy systems need major infrastructure upgrades to allow scalability and improve performance. Moreover, launching APIs for thousands of customers can create a system load leading to performance issues.

Regulatory Framework of Open Banking

The regulatory mandates of various governments are one of the prime forces responsible for the worldwide adoption of the open banking system.

1. PSD2 (Payment Services Directive 2)

One of the initial regulatory mandates was Payment Services Directive 2, or PSD2, a European regulation for electronic payment services that mandates banks to open their payment services and customer data to TPPs, subject to customer consent. The mandate ensures better consumer data protection while encouraging competition, innovation, and security in the payment market.

2. Open Banking in the UK

Another regulatory framework in the UK that enables customers to control their financial data is the Open Banking Implementation Entity (OBIE). It was created by CMA and guides the delivery of APIs, security architectures, and data structures for developers. The guideline ensures that the data sharing and security standards are always met.

Security and Privacy of Open Banking

So, is open banking secure and safe? Here’s what open banking offers in terms of security and privacy.

1. Strong Customer Authentication (SCA)

SCA is a requirement under PSD2. It works like a multi-factor authentication system to verify the customer and safeguard any transaction against fraud.

2. Data Encryption

Data encryption ensures that all financial data are encrypted during transactions. This guarantees unauthorized access to sensitive customer data.

3. Regulatory Compliance

Governments have implemented different regulatory compliances to ensure all operations occur within the framework of compliance. For example, the General Data Protection Regulation (GDPR) in the EU ensures that banks and TPPs comply with the guidelines while handling customer data.

Examples of Open Banking

1. Personal Finance Management Tools

Open banking has given rise to several personal finance management tools that give you a holistic view of your financial situation. It pulls information from all your accounts and shows in a single interface so you know how much you have invested or how much money is left to spend this month.

Having all the customer information on a single platform also benefits banks and financial institutions. It allows them to have a clear insight into the customer's financial situation and offer them more tailored products.

An example of one such financial management tool is Mint.

2. Payment Initiation Services

Payment initiation services are another common example of open banking that allows customers to make an online payment. It is faster, more convenient, and can be done on the go. Consumers can pay directly from their bank accounts through third-party platforms, while merchants can receive the payment without any bank-imposed fees.

An example of such a third-party platform is PayPal.

3. Lending and Credit Services

Open banking has helped speed up lending and credit services, as lenders can view the applicant's financial data and credit history almost instantly. Earlier, the lender had to access different documents from different banks to assess the applicant's creditworthiness. Instant access to banking data has helped lending and credit service providers make quicker decisions and offer more personalized loan and credit products.

An example of such a lending company is Current.

Key Takeaway

Open banking is already revolutionizing the payment industry, and we can only expect to see new innovative solutions in the coming days.

If you, too, want to leverage the benefit of open banking through a payment provider like PayBy then this is your cue.

PayBy offers several payment solutions, such as a payment gateway, virtual wallets and accounts, QR code payments, point of sale, and more, that can suit businesses in industries including insurance, fitness and wellness, hospitals and healthcare, gaming, betting and casinos, and more.

PayBy is licensed by the Central Bank of the UAE and has received the highest financial service approvals to conduct Stored Value Facility (SVF) and Retail Payment Services (RPS) operations. It is also trusted by some of the leading brands in the UAE.

Want to explore more?

Get started today.

Want to know more about cashless payments or how it benefits your business growth?

.svg)

{kind=link}